On 15 July, buy now pay later came under FCA regulation. Most of the preparation across the industry has gone into the lending side: affordability checks, creditworthiness assessments on every transaction including the ones under £50, temporary permissions, the route to full authorisation. That work matters. It is also the part firms could see coming, because it looks like credit regulation and credit teams know how to read it.

The part that gets underestimated is the marketing. From this week, a BNPL promotion is a regulated financial promotion, and it has to clear the same bar as any other credit ad: fair, clear and not misleading, with the key product information shown before the customer commits. For a sector built to convert at the checkout in a single tap, that is a change to how the work gets done, not a line in a policy pack.

What actually changed

Deferred payment credit — the FCA's name for the interest-free BNPL that Klarna, Clearpay and PayPal built the market on — spent years outside the financial promotions regime. The product grew from £60 million in 2017 to more than £13 billion in 2024, with around 11 million UK adults using it inside a single year, and for most of that run the advertising around it was governed by general consumer protection rules rather than the FCA's promotions regime.

Policy Statement PS26/1, published in February, set the final rules and the 15 July go-live. Two consequences land on marketing directly.

Every promotion is now in scope. A communication that invites or induces someone to enter a BNPL agreement is a financial promotion. That covers the "pay in 3" button, the checkout messaging, the in-app nudges, the paid social, the email, and the affiliate and influencer content that sells the option. Each one has to meet the fair, clear and not misleading standard and carry the key product information — the customer's obligations, the amount, the payment schedule, the cash price, the key risks, and whether a credit reference check applies — with the prominence the rules expect.

Consumer Duty sits over all of it. BNPL firms are now subject to the Duty, which raises the standard from "technically accurate" to "delivers good outcomes and supports the customer's understanding". The FCA's April consultation, CP26/15, goes further still, proposing to fold the financial promotions rules for consumer credit into the Duty rather than leaving them under the old CONC 3 regime. The direction is set: promotions get judged on the outcome they produce for the person reading them, and firms are expected to show how they got there.

Which of your promotions are in scope

Close to all of them, which is the point most teams miss when they picture "an ad" and think of a paid campaign.

A BNPL brand does not run one promotion. It runs the checkout copy on hundreds of retailer sites, the option toggles inside the app, the reminder emails, the paid social variants, and a roster of affiliates and influencers pushing the product on commission. Every one of those communications invites someone into a credit agreement, so every one is a financial promotion. The volume is the story here: a single retail integration can put your promotion in front of customers in dozens of contexts you did not individually design.

The affiliate and influencer layer deserves its own line, because it carries a rule that catches firms out. When a third party communicates your financial promotion, someone authorised has to approve it. Under the section 21 regime an influencer post about your "pay in 3" option is a financial promotion that a firm with the right permission has to sign off, against the competence and record-keeping standards the FCA applies to approvers. A creator economy that used to run on a brief and a discount code now runs through an approval gate.

The volume problem

Here is how this plays out inside a marketing function that hasn't changed its process.

A growth team ships promotions the way growth teams do: fast, in variants, across channels, testing what converts. Under the old setup, a "pay in 3" line could go live when marketing was happy with it. Under the new one, each of those communications needs a compliance assessment, the right product information, an approver competent to sign it, and a record of the decision if the FCA asks to see it.

None of those steps is hard in isolation. The difficulty is that there are thousands of them, they change constantly, and the person who ends up holding the sign-off is often a campaign manager with a launch deadline and no view of whether the last version cleared review. When that happens, one of two things follows. Either promotions wait in a queue and the channel that drives the firm's growth slows down, or they go live without a proper check and the firm builds a backlog of communications it cannot stand behind. Both are expensive. The second is the one that shows up in a complaint.

Where the decision should live

Three changes close the gap, and none of them asks marketing to move slower.

Capture the promotion at intake, with its claims and context. The moment a communication enters review, the submission should record what it says, the product terms it relies on, the channel it runs in, and whether a third party is communicating it. Firms already working this way are adding BNPL to an existing discipline; firms starting from a shared inbox have a larger conversation to have first.

Assess it against a house standard, at the speed you publish. The fair, clear and not misleading call and the Consumer Duty outcome test belong in the same review, applied against a documented internal position so the hundredth variant gets the same answer as the first. This is where automation earns its place: software can clear the promotions that plainly meet the standard and route the genuine edge cases to a person, so review runs at the rate the channel demands rather than becoming the bottleneck.

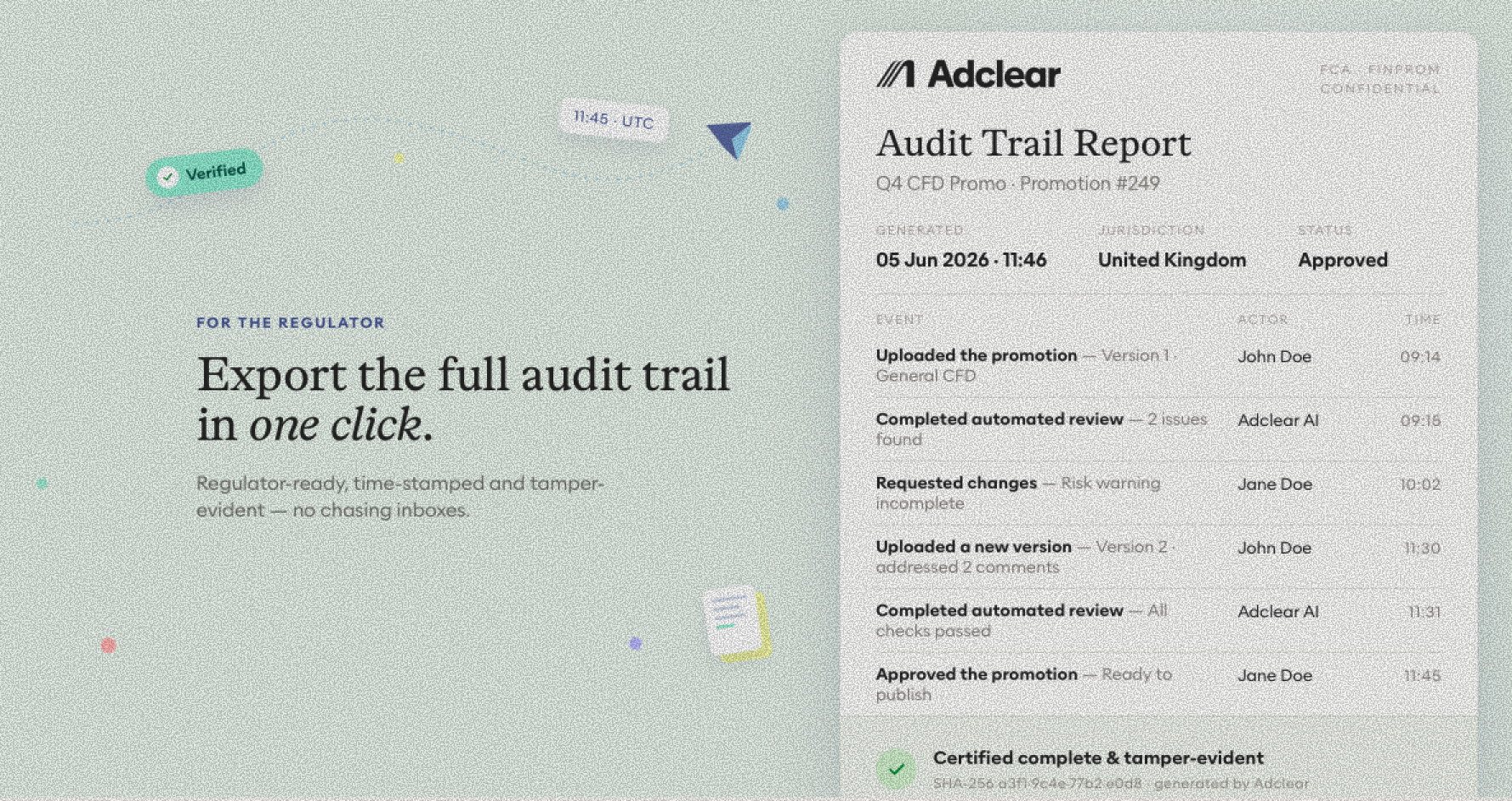

Record the decision where you can retrieve it. What was approved, who approved it, on what basis, and the product information that ran with it, attached to the promotion itself. Consumer Duty and the approver regime both rest on being able to show your working, and an email thread is a record only in the archaeological sense. Firms whose approval records are produced at the point of decision answer a regulator in minutes. Firms reconstructing them from inboxes answer in weeks, at legal rates.

The move this week

The practical first step is an inventory: where do your promotions actually appear, how many communications does that add up to across checkout, app, email, paid and partner channels, who signs each one off now, and where is the record kept. For most BNPL teams that surfaces a number far larger than expected, and it turns an abstract regulatory change into a concrete operational plan.

We've put the full sequence — where promotions live, the scope test, the product-information requirements, the approver question, and the evidence trail — into a working document you can run against your own campaigns. Download it using the form below

Once you're booked in, we'll send you a free playbook on Financial promotions compliance for FinTechs.