The FCA cryptoasset regime treats your admission disclosure as a living document.

Most firms are building it like a launch asset. That gap is where the transition period gets expensive.

Most summaries of the FCA cryptoasset regime stop at the same line. Before you admit a token to trading, you have to publish a cryptoasset disclosure document. It has to explain the asset clearly, carry the information a person needs to make a decision, and avoid misleading statements. That part is being read and understood.

The line that comes next is the one doing the real work, and it keeps getting skipped. If anything material about the asset changes before admission, you have to publish a supplementary disclosure. The document isn't something you write once and file. It's a record you're expected to keep true, and to re-submit to the FCA's central repository when the facts move.

On its own, that reads like housekeeping. Set against how crypto actually behaves, it's a standing obligation most firms coming into the perimeter aren't built for.

Why "material change" triggers constant supplementary disclosures

In equities, a prospectus supplement is an occasional thing. The facts underneath a listed share move slowly and through defined channels. Crypto runs on a different clock. Supply schedules adjust. Governance changes. Backing arrangements, custody providers and third-party dependencies get revised. Listing terms shift as an asset moves across venues. Each of those can be the material change that triggers a fresh supplementary disclosure.

So the obligation the rules describe as an exception becomes something closer to routine. A firm listing a meaningful number of tokens, each with its own disclosure to keep current, is running a continuous maintenance process, whether or not it has named it as one.

The disclosure capability gap crypto firms are underpricing

Traditional finance has maintained regulated documents for decades. Prospectus teams, verification files, sign-off chains, version histories, and a clear record of who approved what and when. The muscle exists because the obligation has always existed.

Crypto-native firms entering the FCA perimeter tend to have deep product and engineering capability and, in most cases, no equivalent communications-compliance function. The regime assumes that machinery is already there. The rules describe the output they want. They don't hand you the process that produces it, and that process is the actual build.

This is the same muscle the financial promotions rules already ask for. Crypto promotions have sat under the financial promotions regime since 2023. The cryptoasset admission disclosure now adds a second, document-level obligation that runs on the same principle. It's a communication about an asset, judged on whether it misleads, that has to be right at the moment someone relies on it. A firm that has never operated a promotions approval function is now being asked to run two overlapping versions of one at once.

What maintaining a cryptoasset disclosure document looks like in practice

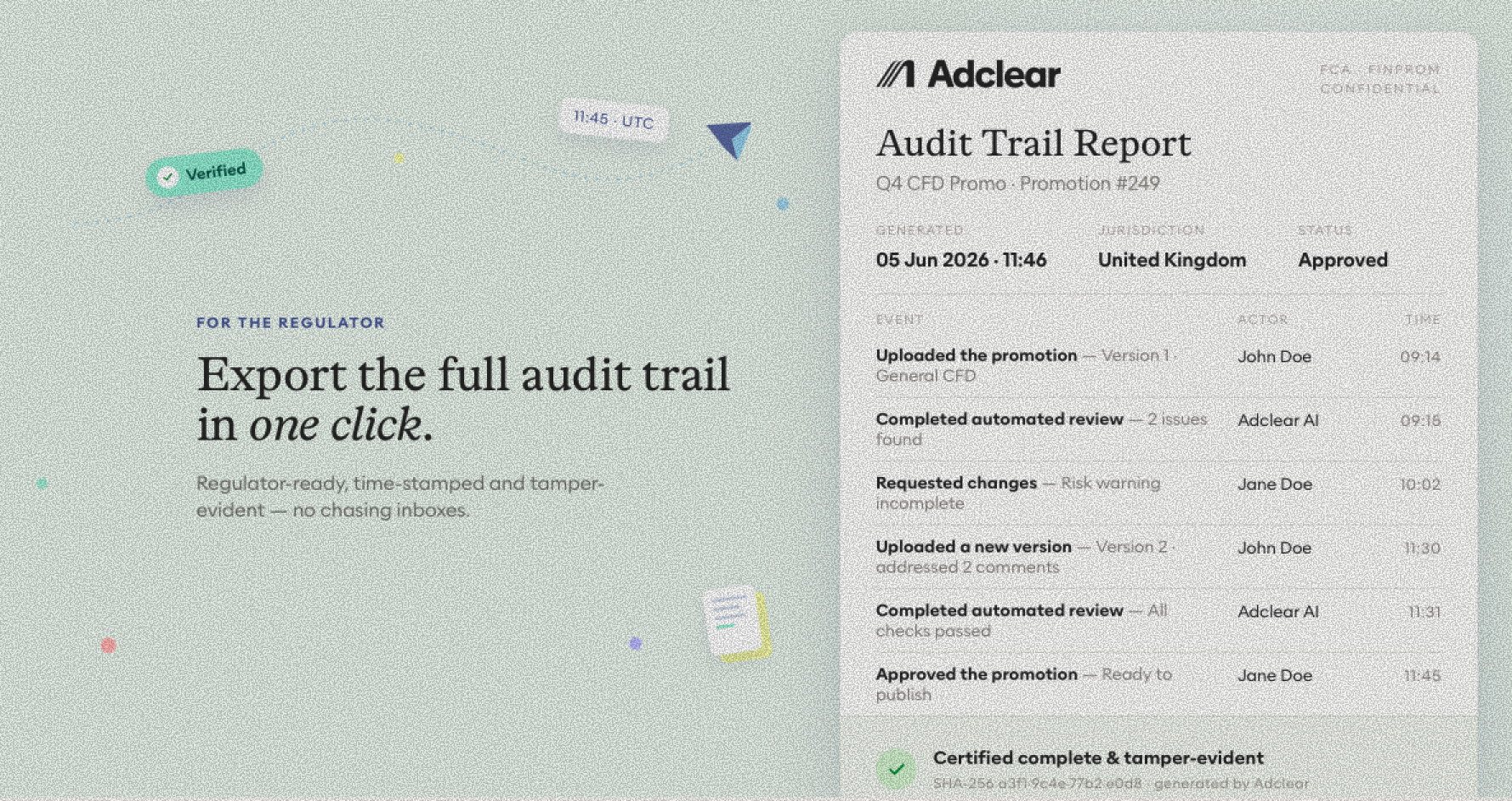

The firms that handle this well will treat the disclosure as a system rather than a file. In practice that means a single source of truth for the current version of every disclosure, so nobody is guessing which draft is live. It means a defined trigger list for what counts as material, agreed between compliance, product and legal before launch rather than argued about after a change. It means a re-approval path that can move as fast as the change itself, because a supplementary disclosure that takes three weeks to clear is a listing that sits in limbo. And it means version history detailed enough to show the exact document that was live on any given date, plus a record of each submission to the repository.

Without that, "supplementary disclosure required" turns into a scramble every time a token changes. With it, the same event is a routine update.

Provability is the standard beneath the FCA's crypto disclosure rules

There's a through-line across the whole regime, from the guidance on applying the Consumer Duty to crypto firms to the admissions rules. It's no longer enough that a communication was compliant in general terms. You have to be able to show it was compliant for the specific version a customer saw, at the moment they acted on it. A disclosure you can't reconstruct by date is a disclosure you can't defend.

That's the real test hiding inside a rule that looks administrative. The firms that build the disclosure as a living, versioned, provable record will spend the transition period creating an asset they can lean on. The ones treating it as a one-off launch task will spend the same period rewriting under pressure and hoping the repository submission matches what actually went live.

Key FCA cryptoasset regime dates

The FCA published its policy statements on 30 June 2026. The authorisation gateway opens on 30 September 2026. The application window for firms already active in the UK closes on 28 February 2027, and firms that miss it risk a transitional "no new business" restriction until they're assessed. The full scope of regulated activities takes effect on 25 October 2027.

The cryptoasset disclosure document isn't the hardest rule in the package to understand. It's the one that keeps running after launch, and the one that rewards the firms who build the process now instead of discovering they need it later.

Frequently asked questions

When does the FCA cryptoasset regime come into force?The FCA published its policy statements on 30 June 2026. The authorisation gateway opens on 30 September 2026, the application window for firms already active in the UK closes on 28 February 2027, and the full scope of regulated activities takes effect on 25 October 2027.

What is a cryptoasset admission disclosure document?It's the document a firm has to publish before admitting a token to trading. It has to explain the asset, carry the information a person needs to make a decision, avoid misleading statements, and be submitted to the FCA's central repository.

What is a supplementary disclosure?If anything material about the asset changes before admission, the firm has to publish an updated disclosure and re-submit it to the repository. In crypto, where the facts underneath a token move often, that turns the disclosure into a document you maintain rather than publish once.

Is a crypto disclosure document a financial promotion?It works on the same principle. It's a communication about an asset, judged on whether it misleads, that has to be accurate at the moment someone relies on it. Firms new to the perimeter also inherit the Consumer Duty, which applies a similar standard to customer communications.

Once you're booked in, we'll send you a free playbook on Financial promotions compliance for FinTechs.