You ship a campaign on a Monday. By Tuesday afternoon, half the ads sit in Policy: Financial Services. The media buyer is emailing compliance. Compliance is emailing legal. The CMO is asking why the Q2 launch window just moved. That's the operating shape of a Google disapproval in an FCA-regulated team, and the damage is rarely in the one rejected ad. It's in the learning cycles you can't run, the budget you can't spend, and the approvals queue that now has to re-review every variant you touch.

On Google specifically, first-time approval is the pinch point most firms measure wrongly. Teams that track only "final approval rate" miss the reality that every re-submission compounds delay. One paid-media lead at a regulated CFD broker puts it as an SLA question, not a creative one: first-time-right, or nothing.

The commercial reality most teams understate

Disapprovals in financial services aren't a copy problem. They're an operating-model problem wearing a policy label.

A mid-size UK fintech running paid acquisition at £400k/month with a 60% first-time approval rate is burning roughly 40% of its creative testing velocity on round-tripping. In one Tier-1 UK bank composite we see repeatedly, 64% of financial promotions were rejected at first submission: nearly two in three ads re-submitted, re-reviewed, re-queued. That isn't a brand risk story. It's a CAC story. Every delayed variant pushes blended CAC up because the winners surface later, the losers sit longer, and the platform's learning phase resets every time you edit a live ad.

The second hit is silent: compliance capacity. When Marketing can only ship through one or two authorised approvers, those approvers become the critical path for every other regulated surface. Product pages, in-app copy, partner material. Google rejections eat that capacity first because they're loudest, so everything else waits.

The six things that actually get ads disapproved

Bottom line: six root causes cover almost every UK financial-services disapproval.

1. UK financial services verification is incomplete. Google's UK rule applies to any advertiser showing financial services ads to UK users, not just those advertising a regulated product. Teams assume verification is only needed for investments or loans. It isn't.

2. The identity chain doesn't line up. Account admin, FCA entity, contact email domain, FRN and advertising domains must all match FCA records exactly. One mismatch and verification fails, and the rejection reason you see on the ad usually blames the copy.

3. The product category needs separate certification or is restricted. CFDs, rolling spot forex and financial spread betting need certification and are limited to specific locations. Binary options are disallowed. Debt services need separate certification. Crypto sits under its own regime. "Financial services" isn't one policy. It's a stack.

4. Required disclosures are missing or poorly presented. Physical address, fees, links to third-party accreditation where affiliation is implied, APR and representative examples for lending products. Google wants these immediately visible, not behind tabs, hovers or extra clicks. This is also where COBS 4.2.1R bites: communications must be fair, clear and not misleading, and FG24/1 has made prominence a named failure mode, not an aesthetic preference.

5. The ad or page triggers misrepresentation. "Best rates", implied guarantees, teaser claims that soften on the page, affiliations that are asserted but not evidenced. Google looks for drift between ad and landing page, and so does the FCA.

6. The destination fails technical review. Redirects, geo-blocks, mobile rendering failures, blocked crawlers, staging-to-live inconsistencies. Compliance can sign off the copy and the ad still dies at the URL.

Why manual review makes this worse at scale

Manual review is fine when you have one market, two approvers, low velocity and mostly evergreen campaigns. It breaks the moment any of those change.

The pattern we see in every scaling UK fintech marketing team:

- Campaigns become reactive to market events or competitor moves.

- Landing pages change weekly because the product team is iterating.

- Multiple jurisdictions mean multiple disclosure standards.

- Affiliates, agencies and lead-gen partners all touch promotional surfaces.

- The same policy judgments have to be made across dozens of assets a week.

At that point, the bottleneck is not "does compliance approve this one." It is "can we apply the same policy interpretation consistently across 80 variants on Friday so Marketing can launch Monday." Manual review does not scale linearly with volume. It scales worse, because each additional reviewer introduces interpretation drift.

Before and after: what changes with pre-submission compliance

Before (manual, reactive): Campaign brief → draft creative → send to compliance approver → 2-3 day review loop → submit to Google → 40% disapproved → re-review → re-submit → learning phase reset. Result: creative reaches optimisation window 10-14 days late.

After (pre-submission checks): Campaign brief → draft creative with policy rules visible to the writer → automated pre-flight against Google + FCA rule set → human review only on flagged items → submit → 85%+ first-time approval → learning phase holds. Result: creative reaches optimisation window inside the same week.

The substance of the change isn't "faster compliance." It's that the compliance rule is visible to the person drafting the ad, at draft time, rather than being applied after the fact. That single architectural change is why first-time approval rates jump, and why compliance capacity frees up for the judgment calls that actually need a human.

The remediation sequence that works

If you are triaging disapprovals right now, do it in this order. Skipping steps is what keeps teams stuck.

1. Pull the exact policy label. Add the Policy details column in Google Ads. Classify into one of five buckets: Verification, Product certification, Disclosure, Misrepresentation, Destination. If your team cannot classify the failure in under two minutes, that is already a workflow problem.

2. Review the landing page before the copy. In regulated categories, the page is the failure point more often than the ad. Check address, fees, risk language, affiliation evidence, geo-access, mobile behaviour, crawler access, and whether the on-page offer matches the ad promise.

3. Clean up the identity chain. FCA entity, Google Ads admin path, contact domain, FRN, all advertising domains, agency/affiliate structure. Google's UK verification explicitly requires exact match with FCA records. Domain hygiene is where most "mystery" rejections live.

4. Rewrite claims last. Remove implied guarantees, drop unevidenced superlatives, align ad wording with the on-page offer, make risk and cost prominent. FG24/1 is blunt: truncated risk warnings in social text and poor digital prominence are named failure patterns.

5. Resubmit, then appeal only if needed. Google's support flow is fix first, re-review, appeal second. Appeals are useful. They are not a substitute for diagnosis.

6. Turn the fix into a rule. This is the step most teams skip. If a campaign failed because a disclaimer was missing, a claim needed evidence, a partner domain was uncovered, or a product category needed certification, codify it as a reusable pre-flight rule. Otherwise you solve it once and repeat it forever.

Objection: "We can't review in 24 hours. Compliance needs days."

We hear this often, and the answer is that pre-submission checks don't remove compliance from the loop. They remove compliance from the 80% of reviews that are repeatable policy checks.

What a 24-hour SLA actually means in a well-run pre-submission setup: automated pre-flight catches the repeatable failures (disclosures, prominence, claim library violations, URL health, domain alignment) before the asset ever reaches a reviewer. The human approver then spends their time on edge cases such as novel claims, new jurisdictions, and unusual products. That isn't faster compliance. That's compliance finally being used where it adds judgment rather than where it catches typos.

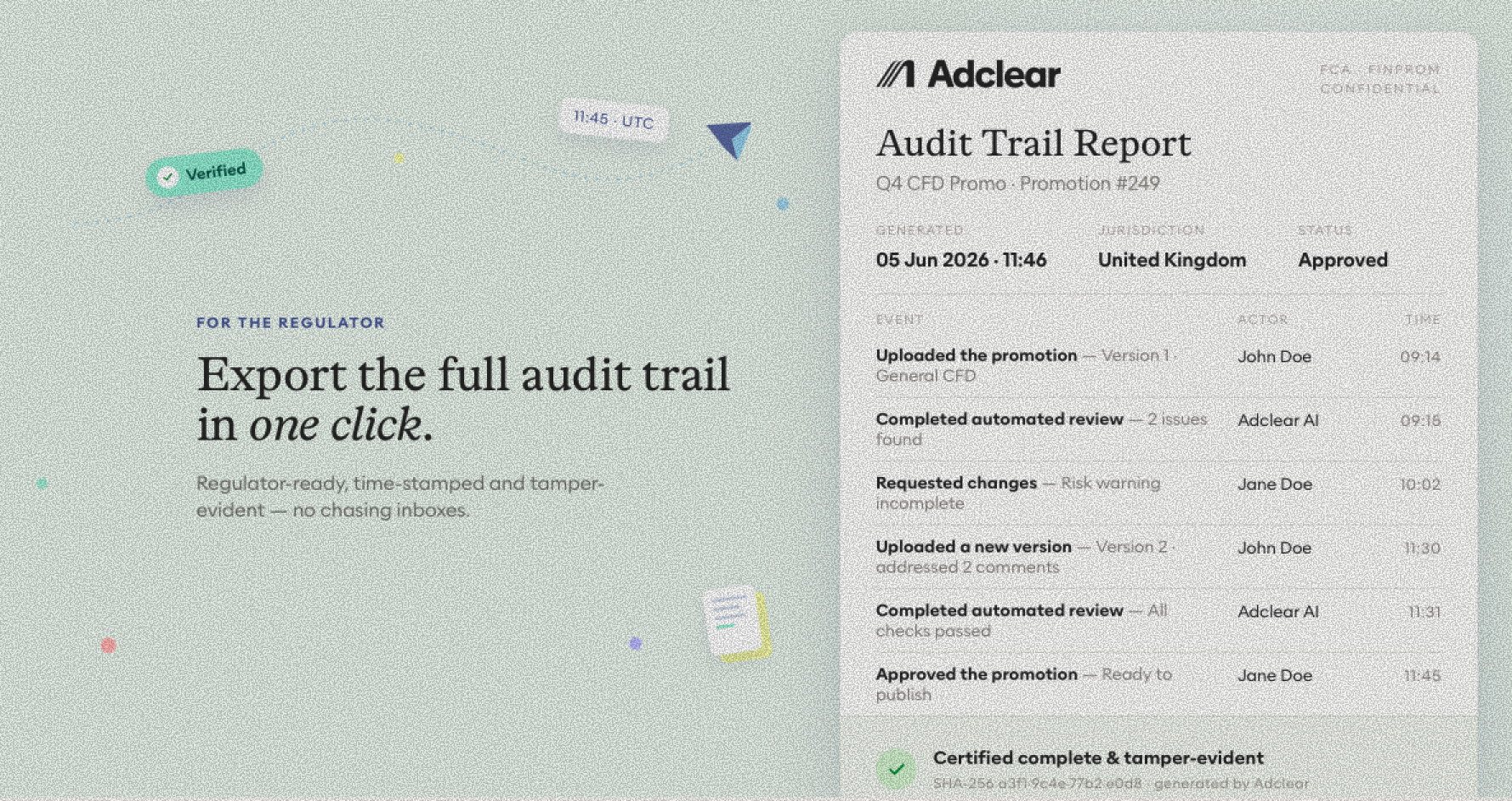

The firms doing this well run 24-hour turnaround on the 80% and keep senior compliance on the 20% that needs it. That is defensible under FCA expectations because the audit trail shows which checks were automated, what rules were applied, and what a human approved and why.

FAQ

Why are my Google Ads for financial services disapproved in the UK?

Usually one of six reasons: UK verification, product certification, landing-page disclosures, misrepresentation, destination health, or identity-chain mismatch. Read the exact policy label in Google Ads before rewriting anything.

Do I need FCA authorisation to run Google Ads for financial services?

Often yes, but not always directly. Google's UK verification covers FCA-authorised firms, approved third parties and certain exempt advertisers. The advertiser still has to fit the right category and complete Google's verification steps.

Can an agency run Google Ads for an FCA-authorised firm?

Yes, but the authorised firm must initiate verification for the approved third party. If the relationship isn't structured correctly inside Google's verification, ads will be rejected even when the agency's work is compliant.

Why does Google reject my ad when the copy looks compliant?

Because Google reviews more than copy. Verification status, product eligibility, landing-page disclosures, destination accessibility, and ad-to-page alignment are all on the review surface. In regulated categories the landing page is often the real failure point.

Can I advertise CFDs, forex or spread betting on Google?

Only in specific locations where the advertiser is licensed and the account is certified. Binary options are disallowed. Treat these categories as separate policy stacks, not "financial services."

Should I appeal or edit first?

Edit first. Google's own sequence is find the reason, fix it, resubmit, then appeal if the decision was incorrect.

Once you're booked in, we'll send you a free playbook on Financial promotions compliance for FinTechs.