AI is genuinely reshaping the financial promotions compliance workflow. The harder question for the compliance leaders actually procuring this technology is which parts of the workflow AI should touch, which parts it shouldn't, and what regulators expect to see when AI sits in the supervisory chain.

The answer is more constrained than most vendor pitches suggest. Some AI use in the workflow is genuinely high-leverage. Some are regulatorily incompatible with current expectations, regardless of model quality.

Three classes of AI use in the workflow

The clearest way to think about AI in financial promotions review is by workflow stage.

Pre-supervisory triage is the highest-leverage application today. Well-designed classifiers can route incoming assets by risk level - touches FINRA 2210, touches SEC Marketing Rule, touches CFPB UDAAP, touches state regimes and escalates only the assets that warrant principal-level review. Done correctly, this preserves human capacity for the cases where judgement is irreplaceable.

In-review augmentation is the moderate-leverage band. Disclosure verification against required language, cross-asset consistency checks, source-of-claim retrieval against substantiation files. AI here is less generative than rule-applying, and it accelerates the reviewer's work without making the supervisory call.

Final approval is the band where AI doesn't fit. FINRA Rule 2210 requires a named human principal to approve retail communications. The SEC Marketing Rule, CFPB enforcement posture, and state-level supervisory standards all converge on the same requirement: named human accountability. An AI system cannot serve as the principal of record, regardless of model quality. Vendors who collapse this distinction are selling a product that cannot survive regulatory examination.

Where AI works today

Three workflow stages benefit clearly from AI right now.

- Intake triage - routing assets by risk level frees senior compliance time for the cases that warrant it.

- Disclosure verification - checking required-language presence, prominence and content against pattern handles the largest single category of remediable issues without consuming reviewer attention.

- Cross-asset consistency - comparing a new asset against thousands of prior approved communications surfaces prior claims and prior disclosure context as the new review happens.

Generative drafting of compliant disclosure language is a fourth application worth mentioning. It produces authored content rather than reviewed content, and any asset using AI-drafted disclosure still requires the full human review pipeline before publication.

Where AI is dangerous

Three workflow stages are not appropriate targets for AI replacement today, for regulatory reasons before technical ones.

The first is final approval, for the principal-accountability reason above. The second is personalisation logic and dynamic content: communications whose final delivered form varies by audience, signal, or time. The asset reviewed at approval may not be the asset that reaches the consumer; AI can instrument the system but cannot certify the eventual delivered communication on its own. The third is contextual or commercial judgement. This includes novel product categories, communications touching live litigation, anything where the regulator will eventually ask what the human thought at the time.

Vendors pitching end-to-end AI review without a named principal in the chain are selling a product that will not survive regulatory examination. Compliance leaders should treat that pitch as a disqualifying signal.

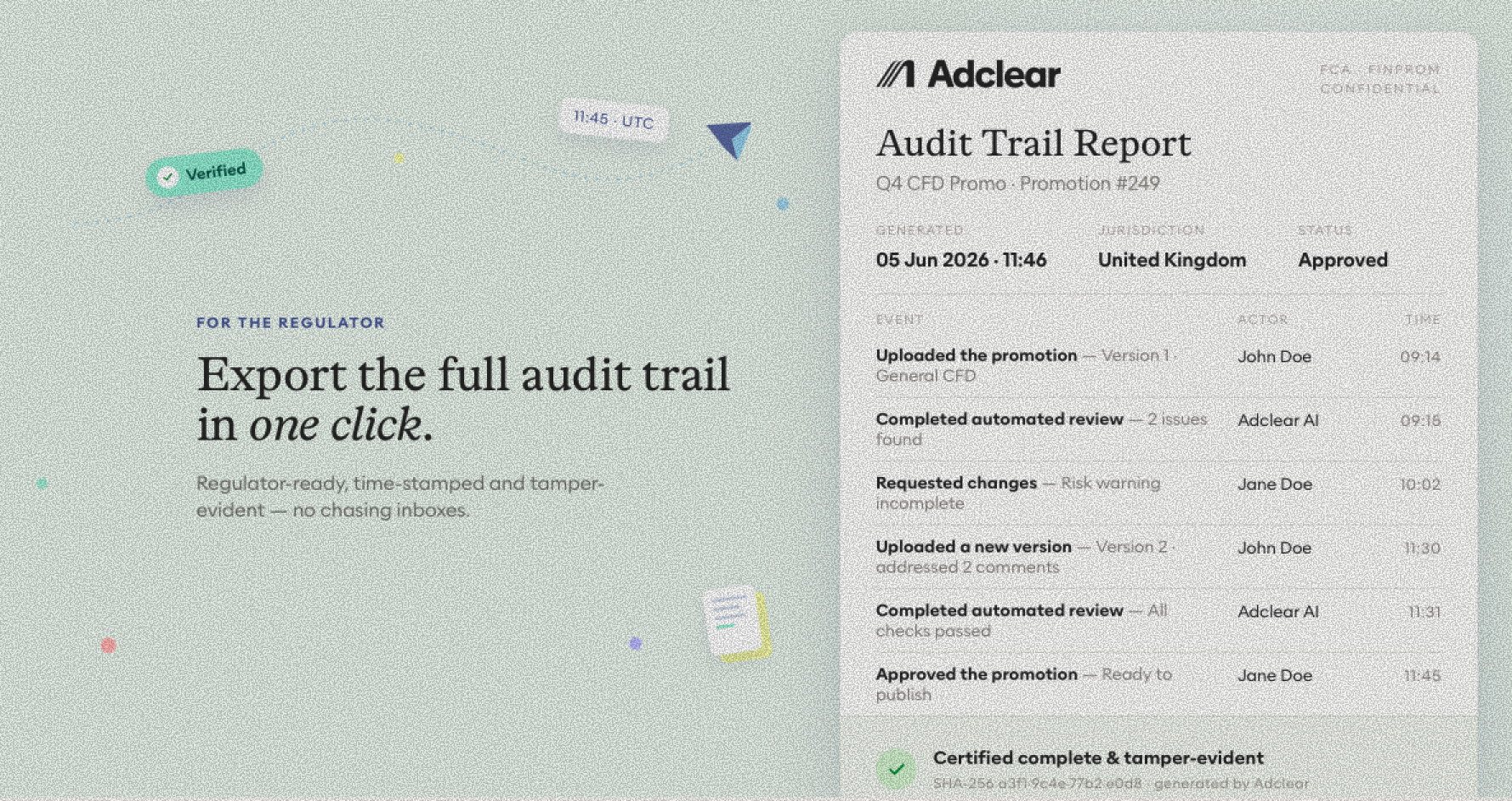

Documenting AI-assisted review for regulators

If AI is in the workflow, the supervisory record needs to reflect it. The minimum documentary standard includes the model and version used, the inputs supplied to the model, the model's outputs captured rather than summarised, the human principal's notes on which outputs were accepted and which were overridden, and the final decision attached to the named principal.

A firm that produces this record for every asset is operating to current regulatory expectations regardless of how aggressively it uses AI. Without that record, the firm carries exposure even when its AI use is conservative.

How Adclear fits

Adclear is the AI compliance platform for marketing and communications, designed around the human-in-the-loop architecture that regulatory examination requires. AI accelerates the volumetric work - intake triage, disclosure verification, cross-asset consistency, drafting assistance - while the supervisory principal owns every approval decision.

Every AI output is captured automatically as a supervisory artefact, attached to the principal's review trail. This is what allows a firm to scale AI use aggressively without diluting the supervisory record, and what allows the firm to answer the next examiner's question on AI use in compliance review.

Talk to us

Adclear is hosting the Chicago stop of our Front Row series on Thursday June 11 - an off-the-record breakfast with senior US compliance leaders, with a panel on this exact question: AI in compliance, signal vs hype. Panel led by Ed Ryan (Chief Compliance & Operating Officer, Ironbeam) and Jeremy Dela Cruz (Conduct & Communications Lead, NinjaTrader). Request a seat at www.luma

FAQ

Can AI replace human review in financial promotions compliance? Not for final approval. FINRA Rule 2210 requires a named human supervisory principal. AI can accelerate the workflow at every other stage, but it cannot replace the principal of record.

What documentation is needed when AI is in the workflow? The model and version used, the inputs supplied to it, the outputs the model produced, the human principal's notes on which outputs were accepted or overridden, and the final approval attached to the named principal. Each captured at approval time, not reconstructed afterward.

How do regulators view AI-assisted compliance review today? No formal AI-specific guidance for financial promotions has been issued yet. Existing regulation (FINRA 2210, SEC Marketing Rule, CFPB enforcement posture) already imposes named-human-accountability requirements that constrain how AI can sit in the workflow. Mature firms are operating ahead of formal guidance.

Adclear is the AI compliance platform for marketing and communications — pre-publication review and post-publication monitoring across ad copy, social, affiliates, client communications, and investment material. Three years of UK FinProm operating experience; US launch June 2026.

Once you're booked in, we'll send you a free playbook on Financial promotions compliance for FinTechs.